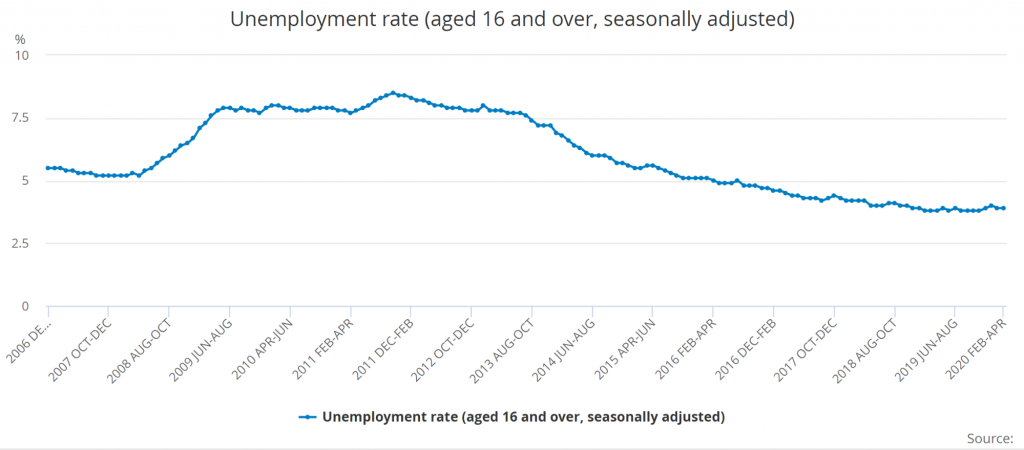

In its latest unemployment report, the Office of National Statistics reported that the rate of unemployment in the UK rose to 3.9%, an increase of 50,000 people in unemployment.

That figure was from the start of the pandemic, and the number of those unemployed is likely to be much larger due to Covid-19. When many people file for unemployment, the number of those requiring UK unemployment benefits will also rise. This article will provide an overview of the help and benefits available in the UK if you find yourself without a job.

Unemployment rate (age 16 and over) Jan 2007 – Apr 2020; Source: ONS

It is important to remember that claiming UK unemployment benefits is a good thing. It is there for a reason and the stigma that sometimes surrounds it should not hold you back from seeking help.

What UK Unemployment Benefits Are Available?

Jobseekers’ Allowance (JSA)

If you become unemployed, your first port of call is JSA. This is available to you while you look for a full-time job or if you’re working less than 16 hours a week.

The three types of JSA are:

- Contribution-based

- ‘New style’ JSA

- Income-based

Basic eligibility criteria for JSA:

- You must be 18 or over and under the pension age

- You work less than 16 hours per week

- You are available for full-time work and are actively looking for it

- You are not in full-time education

- You are not claiming Income Support

- You do not have an illness or disability that prevents you from working

Contribution-based JSA (CBJ)

Contribution-based JSA is the best option as your savings, assets and partner’s income won’t affect the calculation or amount of your claim. You can claim CBJ, irrespective of your citizenship.

To claim CBJ, you need to have:

- Worked for at least 26 weeks earning more than the lower earnings limit (£120) per week for at least one of the last two years

- Paid Class 1 National Insurance on 50 weeks’ work at the lower earnings limit during each of the 2 previous tax years

Furthermore, you can only apply for CBJ if you get either:

- The severe disability premium, or

- Received or were entitled to the severe disability premium in the last month and are still eligible for it.

New-style JSA

To be eligible, you’ll have to have worked as an employee for at least 26 weeks earning more than £120 a week in at least one of the 2 previous tax years. You must have paid Class 1 NI contributions for the last 2 to 3 years.

You also need to meet these criteria:

- Be 18 or over

- Be under pension age

- Not be in full-time education

- Be available for work

- Not be working at the moment, or working less than 16 hours a week

- Not have an illness or disability which stops you from work

- Live in England, Scotland or Wales

- Have the right to work in the UK

You must also actively be seeking full-time employment.

Income-based JSA

Universal credit has replaced income-based JSA for most people.

You can only apply for income-based JSA if you either:

- Get the severe disability premium, or you are entitled to it, or

- You got or you were entitled to the severe disability premium within the last month and you are still eligible for it

You also need to meet these eligibility criteria for income-based JSA:

- Be 18 or over

- Be under pension age

- Not be in full-time education

- Be available for work

- Not be working at the moment, or working less than 16 hours a week

- Not have an illness or disability which stops you from work

- Be single or have a partner that works less than 24 hours a week on average

- Have £16,000 or less in savings (this includes your partner’s savings)

If you have a partner and are claiming income-based JSA, you must make a joint claim. For further information, go to your nearest Jobcentre or Jobcentre Plus.

How Much JSA Will You Get?

Every type of JSA pays the same personal allowance per week. The amount is dependent on your age:

- 18 to 24 – £58.90

- 25 or over – £74.35

- If you claim income-based JSA as a couple, you can get £116.80

However, the exact amount you get depends on your circumstances, so it’s impossible to provide an accurate number here. The Turn2Us Benefits Calculator can help you calculate your JSA entitlement.

You may also receive extra payments called premiums if you claim income-based JSA and you or your partner are:

- Disabled

- A carer receiving Carer’s Allowance

- Over the state pension age for a woman

How to Claim Jobseeker’s Allowance?

The easiest method is through Jobcentre Plus. To find your nearest Jobcentre, follow this link.

Alternatively, you call them on 0800 055 6688 or 0800 023 4888.

For more information on JSA and other UK unemployment benefits available, visit the Government website.

Support for Mortgage Interest (SMI)

Alongside your JSA, you may claim SMI if you are a homeowner who requires help towards mortgage payments of up to £200,000. This becomes £100,000 if you are getting pension credit or any other qualifying benefit.

The SMI is a loan that you borrow from the Government to pay your interest on your existing mortgage or to pay for loans that you have taken out for certain repairs and improvements on your home. The payments go directly to your lender.

You do not have to pay back the loan immediately – only once you sell your home or transfer ownership of it to another. Interest is added to your loan, currently at a rate of 1.3%.

To qualify for SMI, you need to be getting one of these:

- Income support

- Income-based JSA

- Income-related Employment and Support Allowance

- Universal Credit

- Pension Credit

SMI cannot be used to:

- Repay the amount you borrowed

- Pay anything towards insurance policies you have

- Pay missed mortgage payments

Universal Credit (UC)

Those who are out of work, on a low income or those who cannot work are paid Universal Credit. It is a payment to help with your living costs and is paid out monthly or twice a month.

To apply, click here, create an account and complete the form.

Universal credit has replaced the following benefits:

- Child tax credit

- Housing benefit

- Income support

- income-based JSA

- Income-related Employment and Support Allowance

- Working tax credit

You can’t claim UC if you get a severe disability premium or are entitled to it or you got or were entitled to the severe disability premium in the past month and are still eligible for it.

You can claim UC if you are:

- On a low income or out of work

- Over the age of 18

- Under the state pension age (or if your partner is)

- With savings under £16,000 between you and your partner

- Living in the UK

How much UC with you get?

While we cannot calculate exactly how much you will get, these are the standard amounts:

| Circumstance and Age | Standard UC Amount |

| Single, under 25 | £342.72 per month |

| Single, over 25 | £409.89 per month |

| Joint claim, both under 25 | £488.59 per month |

| Joint claim, one or both over 25 | £594.04 per month |

This is merely the basic rate, if you require further help with housing, children, childcare, caring for another or for not being able to work due to sickness or disability, then extra amounts can be added to your standard amount.

The more you earn, the less UC you receive. For every £1 you earn, you typically lose 63p in UC. However, if you have a child, you can work a little bit without reducing your UC amount.

How the UC payment works?

After you apply, it usually takes 5 weeks to get your first UC payment. But you can ask for advance payment if you don’t think you will have enough to live on for those 5 weeks.

After the initial payment, you will be paid every month on the same date.

If you receive UC to pay for housing, you will be expected to pay this yourself but it will come separately, called the ‘housing element’.

Backdating UC

You can backdate your payment for up to 1 month before you started your claim. But you need to demonstrate to the Department for Work and Pensions (DWP) that you had a good reason for not claiming earlier.

For example:

- Illness – you need a medical certificate

- Disability

- You were not told that your JSA/ESA was going to end

- The online claims system was down

- You have broken up with your partner and are now making a single claim

- You did not claim in time because DWP gave you the wrong information

Your Responsibilities for Claiming UC

UC comes with responsibilities that you must agree to when you apply. Primarily, this is to look for a job, but this can be split into:

- Writing a CV

- Actively looking and applying for full-time jobs

- Seek training to develop your skills

You must also pay your own rent and other housing costs that may be accrued as well as reporting any changes to your circumstances. If you fail to report any changes to your circumstances, you may face a £300 fine.

If you do not meet these responsibilities, you may receive a sanction. Sanctions are a punishment for not doing your part. One such sanction may be to end your UC payment or reduce it by a certain amount.

If your payment is stopped through a sanction, you can ask for a hardship payment if you can’t pay for rent, heating, food and hygiene needs. You will have to repay this through future UC payments. To receive hardship payments, you need to show:

- That you tried to find the money from somewhere else

- That you only spent the money on essentials

Food Bank

Food banks are the last resort if you do not have any money for sustenance. Use the internet, local job centres or Citizens Advice to find where your local food bank is.

However, most food banks do not allow walk-ins – often, you need a referral. The best place to get a referral is your local Citizens Advice who will assess your situation and refer you.

Find your nearest Citizens Advice by clicking here. Alternatively, call their advice line through this number: 03444 111 444 (England) or 03444 77 20 20 (Wales).

UK Unemployment Benefits for EEA Citizens

You may be able to claim benefits if you are from the EEA and have a right to reside in the UK or have settled status. The EEA covers the EU member states as well as Iceland, Liechtenstein, and Norway. Swiss nationals, while not from within the EEA, may be able to claim some benefits.

- If you’ve lived in the UK for longer than 5 years, you need to apply for ‘settled status’ in order to be eligible to receive benefits.

- If you’ve lived in the UK for less than 5 years, you may be eligible for some benefits, but you need to apply for ‘pre-settled status’. You will need to prove that you have a right to reside in the UK and that the UK is your main home.

Right to Reside

Someone may have a right to reside if you are:

- Working – here you need to prove you’ve earned an average of £183 per week for the past three months and will need evidence to show that you are working. For example, tax documents, contracts or communication with your employer.

- Self-employed – here you need to prove you’ve earned an average of £183 per week for the past three months. You need to produce evidence that you are self-employed. If you are recently self-employed, evidence of finding work may be sufficient – e.g. advertising your business or services.

- A job seeker – you can claim child benefit if you can prove that you are actively looking for work. If you’ve had to stop working because you were made redundant or it was difficult to keep working, you may be able to retain your worker status if you prove that you are actively looking for a job.

- Pregnant and stop working – you can keep your right to reside if you are on maternity leave. In this case, you retain your worker status for up to one year.

- Ill or have been in an accident – you need a ‘sick note’ from your doctor and prove that you will be well enough to work in the future in order to retain your right to reside.

- A student or self-sufficient – you have a right to reside if you are self-sufficient and are unlikely to be a burden on the social assistance system.

- With a family member with the right to reside – you will have the same rights as a family member who has a right to reside. Family members can be:

- Husband, wife or civil partners

- Parents or grandparents and depend on them to live

- Child or grandchild if you depend on their support to live

Permanent Right to Reside

You may have a right to permanent residency in the UK if you’ve spent five years in the UK as:

- a worker or self-employed person

- someone who has stopped working but kept their worker status

- a jobseeker

- a self-sufficient person

- a self-sufficient student

- the family member of someone with a right to reside

UK Unemployment Benefits Available to Non-EEA Citizens

You cannot claim the majority of UK unemployment benefits if you are a person subject to immigration control.

You are a person subject to immigration control if you are not an EEA citizen and you fall into one of these categories where you:

- Need permission to enter or remain in the UK and do not have it

- Have permission to enter or remain in the UK on condition that you have no recourse to public funds

- Must leave to enter or remain in the UK as a result of someone providing a maintenance undertaking

You may claim the following UK unemployment benefits regardless of your immigration status:

- contributory benefits – contribution-based Jobseeker’s allowance or contribution-based employment and support allowance.

- statutory payments – such as sick pay, maternity, paternity or shared parental pay.

- maternity allowance.

- industrial injuries benefits.

To be able to claim, you may need to further satisfy the residence and presence rules.

UK Unemployment Benefits Unique to Covid-19

Furlough Scheme

Your employer may choose to furlough you if they cannot pay you or if there is no work to be done. Alternatively, you can ask to be furloughed if you are:

- Vulnerable and want to ‘shield’ or you live with someone who is vulnerable

- For further information on shielding, follow this link to the UK government’s directives

- Looking after your children while the schools are closed

- Pregnant or have another health condition that you are worried about

- Over the age of 70

Through the government’s furlough scheme, you will be paid 80% of your normal pay up to a maximum of £2500 a month. To receive money through the scheme, your employer needs to apply – if they haven’t explicitly mentioned it, check that they have. According to the BBC, this scheme has been extended until Septemeber 2021.

Furlough Eligibility

Your employer can only use the scheme to pay you if you’ve already been furloughed prior to 11 June 2020, or you’re returning from adoption, paternity, parental, parental bereavement or maternal leave.

You may also be furloughed full time or part-time.

But, remember – you do not have a right to be furloughed, it is up to your employer.

As government advice is revised and changed weekly, please track UK Government guidance pages for both employees and employers so that you can access the most up to date information.

Your Rights if Your Employer Becomes Insolvent

If your company is wound up, then most likely, you will lose your job. In case a liquidator is appointed by the court, then your contract will automatically be terminated. On the other hand, if the company is voluntarily wound up and a liquidator is appointed independently, they can choose whether to terminate your contract.

In these cases, the liquidator is only responsible for the rights that you have accrued since he has been appointed as a liquidator. If there are any existing rights that you believe have been infringed, such as employer pension contributions, then your issue is with your previous employer, not the liquidator.

If you are dismissed because of insolvency, then you may be owed:

- basic pay

- overtime

- maternity pay

- holiday pay

- bonuses, commissions

- redundancy pay

- sick pay

You may be able to recover some or all of the money you are owed depending on whether there are other creditors. In this case, you have a few options available:

- If you want to bring an action against your company, before they apply to be wound down, you should write to Companies House to inform them that you are owed money by the employer. However, only do this if you are prepared to take your case to a tribunal. These can incur heavy charges and should only be done if you are owed significant amounts of money.

- If a liquidator is appointed, you can use them to recover your money owed from the Redundancy Payments Service, if it is a debt covered by it. Alternatively, you can register as a creditor of the company, although it is unlikely that you are given priority in repossessing the debt.

- If no liquidator is appointed, you cannot access the Redundancy Payments Service, but you can sue your employer to gain the money back. However, when claiming statutory redundancy pay, you can still claim it from the Service.

Redundancy Pay

We will provide an overview of what you can claim if you have been made redundant.

There are two types of redundancy pay:

- Statutory redundancy pay – what the Government says that you are entitled to.

- Contractual redundancy pay – extra money on top of the statutory pay that is stipulated in your contract.

You will receive redundancy pay if you:

- Have been employed for at least 2 years, continuously.

- Have lost your job because there was a genuine need to make redundancies in your workplace.

- Are an employee – this includes part-time employees. Follow this link to check your redundancy pay status if you are an employee.

If you are entitled to redundancy pay, you should receive this automatically and within a reasonable time frame. If your employer fails to or denies to pay you, then you can bring the matter to a court for them to decide.

You will not get statutory redundancy pay if you are:

- Self-employed

- Serving in the police or armed forces

- A Crown servant or civil service officer

- A share fisherman/woman

- Working for your immediate family as domestic staff

- An employee of a foreign government

- Working in your job for less than two years

You may also lose your right to statutory redundancy pay if you:

- Turn down an alternative job offered by your employer without good reason,

- Attempt to leave before the job has ended,

- Are fired for gross misconduct before the job has ended.

Where you cannot claim statutory redundancy pay, you may still be able to receive contractual redundancy pay – so always check your contract for further information.

What is the Redundancy Pay You are Entitled to?

Working out the amount of redundancy pay you are entitled to is complicated. Luckily, the Government has provided a calculator to make the process easier. To use it, you will need to know the following:

- The date you were made redundant

- How many full years you have worked for the employer (years of service)

- Your weekly pay before tax.

The redundancy pay is based on how long you have worked for your employer and your age when you worked for them.

For each full year that you have worked for your employer, you get:

- Half a week’s pay if you are between the ages of 18 and 22

- One week’s pay if you are between the ages of 22 and 40

- 1.5 weeks’ pay if you are over the age of 41

This is subject to some limits:

- The maximum weekly amount you can get is £538, even if you earn more per week.

- Your length of service is capped at 20 years.

Backdating Your UK Unemployment Benefits

Backdating benefits is when you claim UK unemployment benefits that you would have been eligible for in the past. Benefits can be backdated in these circumstances:

- You were entitled to the benefit before the date on which you made the claim (a late claim). The time limit for backdating benefits is usually restricted to three months prior.

- If a decision is reversed or overruled, you may be eligible to claim payment of any arrears of benefit.

- After a successful appeal, you may be eligible to claim the arrears of benefit.

If you do find yourself unemployed, there are many unemployment benefits in the UK available. It is always wise to check what you are entitled to using the Turn2Us benefits calculator or by contacting Citizens Advice.